When the Market Gets the Story Wrong: What Oil Teaches Us About Broken Assumptions

Even expert forecasts can fail when their assumptions about demand, supply, and transition speed don’t match reality. The oil market shows how consensus thinking can break down—and why investors should focus less on predictions and more on hidden assumptions behind them

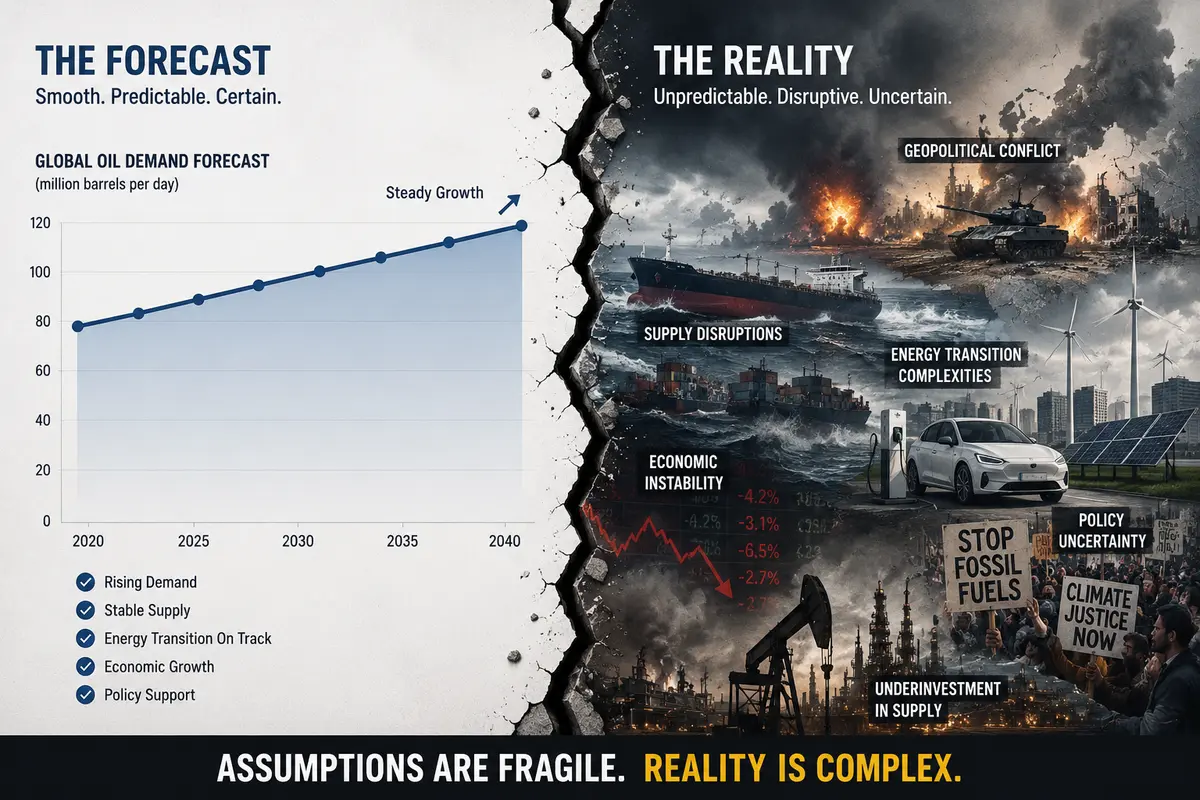

When Experts Get It Wrong: What Oil Teaches Us About Market Assumptions

Every investing era has its “obvious truth.”

For a long time, one of those truths was simple:

Oil demand will steadily decline, and prices will stay structurally weak.

Many respected forecasts—including those discussed in outlets like The Economist—leaned toward this view. The logic looked airtight:

- Electric vehicles are rising

- Renewable energy is getting cheaper

- Efficiency is improving

- Governments are pushing decarbonization

So the conclusion seemed inevitable: peak oil demand is near, maybe already behind us.

And yet, oil prices did not behave politely.

Instead of a smooth decline, we got volatility, spikes, shortages, and repeated “surprises.”

So what went wrong?

1. The market assumes smooth transitions (but reality is jagged)

A key mistake in many forecasts is assuming linear change.

Experts often model energy transition like this:

“Oil demand declines 1–2% per year.”

But real systems don’t behave like spreadsheets.

What actually happens:

- Demand stays sticky longer than expected

- Supply investment drops faster than demand

- Geopolitical shocks disrupt production

- Underinvestment creates sudden shortages

The result is not smooth decline—it is sharp imbalance cycles.

Markets don’t price smooth stories. They react to scarcity shocks.

2. The “replacement assumption” is always too optimistic

A common hidden assumption was:

“Renewables and EVs will replace fossil fuels quickly enough to offset demand.”

This is where forecasts often drift from reality.

Even if EV adoption grows fast:

- Aviation still needs jet fuel

- Shipping still depends on oil derivatives

- Petrochemicals remain deeply oil-based

- Emerging economies still increase total energy consumption

So the real assumption failed here:

Analysts assumed substitution would be faster than system-wide growth in energy demand.

In other words, they underestimated how big the baseline demand actually is.

3. Supply side surprises matter more than demand forecasts

Most long-term oil models focus heavily on demand.

But oil prices are often dominated by supply shocks:

- OPEC production decisions

- Wars and sanctions

- Underinvestment in new fields

- ESG-driven capital withdrawal from fossil fuels

Even if demand is predictable, supply is not.

This is where even strong institutions misjudge the system.

Because supply behaves like a political variable, not an economic one.

4. The biggest trap: believing consensus is “priced in”

This is where your Klarman-style thinking becomes powerful.

When “everyone agrees” on a future, markets often behave like:

“It must already be reflected in prices.”

But consensus narratives can still be wrong.

Oil is a perfect example:

- Many believed demand was clearly peaking

- Capital stopped flowing into exploration

- Yet demand remained resilient

- Supply tightened instead of demand collapsing

So the market didn’t misjudge one number—it misjudged the timing and direction of constraints.

5. Why even experts get trapped

It’s not that experts lack intelligence.

It’s that they are often working with models that assume:

(a) Stability

Markets are rarely stable.

(b) Rational investment cycles

Capital investment in energy is highly emotional and policy-driven.

(c) Gradual adjustment

Reality often adjusts in bursts.

(d) Complete information

But energy systems are full of hidden variables:

- geopolitical risk

- regulatory shifts

- infrastructure bottlenecks

So even sophisticated models break when the system shifts regime.

6. The deeper lesson: markets don’t price truth—they price narratives

This is the key takeaway.

The market is not asking:

“What is objectively true about oil demand?”

It is asking:

“What do we believe most participants believe about oil demand?”

And that second question is unstable.

Because narratives change faster than fundamentals.

7. What this means for investing

This connects directly to one's “market expectations” idea.

For any stock or sector, the real analysis is:

Step 1: Identify the dominant narrative

Example:

- “AI demand will grow exponentially”

- “EVs will kill oil demand”

- “Interest rates will stay high”

- “Cloud spending will accelerate indefinitely”

Step 2: Ask what assumptions are embedded inside it

- growth rate expectations

- margin expectations

- capital spending cycles

- competitive stability

Step 3: Look for fragile assumptions

The weak points are usually:

- timing assumptions (“this happens in 2 years”)

- linear extrapolations

- ignored supply constraints

- ignored capital cycles

Step 4: Ask what would cause a regime shift

Not a small miss—but a structural change in belief.

Closing thought

Oil is not really a story about energy.

It’s a story about how intelligent people can still be wrong when they assume:

- the future will be smooth

- consensus is stable

- systems behave like models

The uncomfortable truth is:

Markets don’t fail because people are irrational.

They fail because reality is more complex than the assumptions inside the models.

Sources: 1. We woz wrong about oil - From The Economist dated Jul 2nd 2026

Leave a Comment

Comments